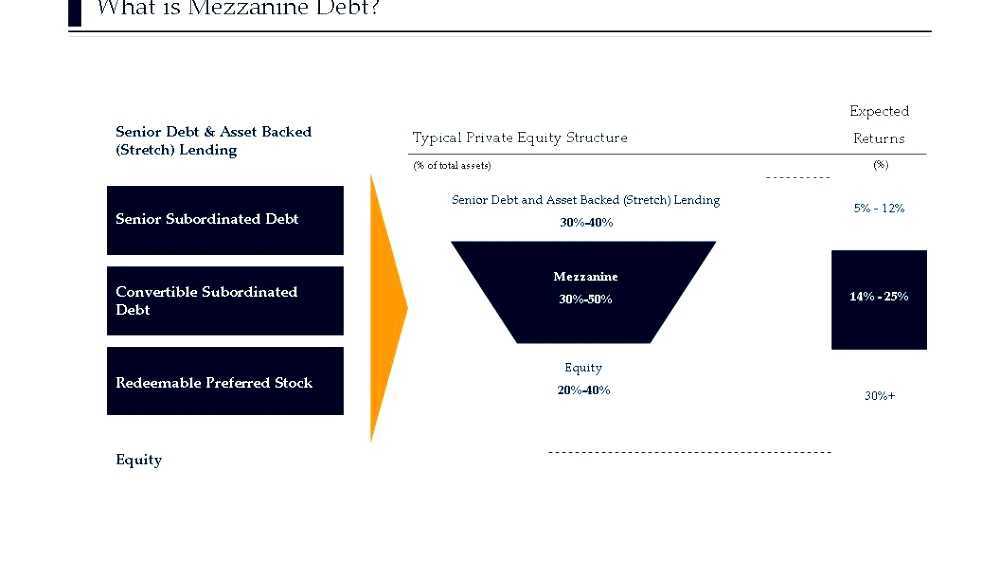

In finance, mezzanine capital is a subordinated debt or option equity instrument representing a claim for a company's only senior assets of common stock. Mezzanine funding can be well structured as debt (usually in the form of unsecured and subordinated records) or preferred stock.

Mezzanine capital is often a more costly source of financing for companies than secured debt or senior debt. The higher capital costs associated with mezzanine financing are the result of an unsecured, subordinated (or junior) obligation in the company's capital structure (ie, in the event of default, mezzanine financing is paid only after all senior obligations are satisfied). In addition, mezzanine financing, which is usually a private placement, is often used by smaller companies and may involve greater overall leverage than the high yield market issue; they thus involve additional risk. As compensation for the increased risk, mezzanine debt holders require higher returns for their investment than guaranteed or more senior lenders.

Video Mezzanine capital

Structure

Mezzanine funding can be accomplished through different structures based on the specific objectives of the transactions and on-site capital structure. The basic forms used in most mezzanine supplies are subordinated records and preferred stock. Mezzanine lenders, usually a special mezzanine investment fund, are looking for a certain rate of return that can be derived from (each individual's security may consist of one of the following or a combination thereof):

- Cash Flowers: Periodic cash payments based on a percentage of the mezzanine loan balance. The interest rate can be either fixed during the loan term or may fluctuate (ie, float) along with LIBOR or other base rate.

- Interest in PIK: Interest-bearing debt is a form of periodic payment in which interest payments are not paid in cash but by increasing the principal amount by the amount of interest (for example, $ 100 million bonds by 8% PIK interest rate will have a balance of $ 108 million at the end period, but will not pay any cash interest).

- Ownership: Along with typical debt-related payments, mezzanine capital often includes equity shares in the form of attached warrants or conversion features similar to convertible bonds. The ownership component in securities of an attic is almost always accompanied by PIK cash or interest, and, in many cases, by both.

Mezzanine lenders also often charge a regulatory fee, payable in advance on the closing of the transaction. Regulatory fees contribute the smallest return, and their purpose is primarily to cover administrative costs or as an incentive to complete transactions.

The following is an illustrated example of mezzanine financing:

- $ 100 million of senior subordinated notes with warrants (10% cash interest, 3% PIK interest and warrants represent 4% of fully attenuated ownership of the company)

- $ 50 million preferred stocks redeemable with warrants (0% cash interest, 14% PIK interest and warrants representing 6% of fully attenuated ownership of the company)

In managing mezzanine security, companies and lenders work together to avoid burdening the borrower at full interest cost of the loan. Because the mezzanine lender will seek a 14% to 20% refund, this return must be accomplished by means other than simple cash interest payments. As a result, by using ownership of shares and interest on PIK, mezzanine lenders effectively refuse compensation until the security due date or change of control of the company.

Mezzanine funding can be done either at the enterprise operating level or at the parent company level (also known as structural subordination). In the parent company structure, because there is no operation and therefore no cash flow, the structural subordination of the security and reliance on the cash dividends of the operating company introduces additional risks and usually higher costs. This approach is taken most often as a result of the existing corporate capital structure.

Maps Mezzanine capital

Usage

Leveraged buyout

In leveraged buyouts, mezzanine capital is used in conjunction with other securities to fund the acquisition price of the acquired company. Typically, mezzanine capital will be used to fill the financing gap between cheaper forms of financing (eg senior loans, second lien loans, high yield financing) and equity. Often, financial sponsors will spend other sources of capital before switching to mezzanine capital.

The financial sponsor will seek to use mezzanine capital in leveraged purchases to reduce the amount of capital invested by private equity firms; since mezzanine lenders usually have lower capital cost targets than private equity investors, using mezzanine capital can potentially increase the return on investment of private equity firms. In addition, medium-sized companies may not be able to access high-yield markets due to their high minimum-size requirements, creating a need for flexible personal mezzanine capital.

Real estate finance

In real estate financing, mezzanine loans are often used by developers to secure additional financing for development projects (usually in cases where the primary mortgage or construction loan equity requirement is greater than 10%). These kind of mezzanine loans are often secured by the second rank of real property mortgages (ie, ratings under the first mortgage lender). The process of standard mortgage foreclosures can take more than a year, depending on the relationship between the first mortgage lender and the mezzanine lender, which is governed by the Accountant Deed.

See also

- Capital growth

- High yield debts

- The history of private equity and venture capital

- Hybrid Security

- PIK Loans

- Secondary equity private market

- Private equity

- Senior debt

References

External links

- What is Mezzanine Debt

- Mezzanine Finance - White Paper

- List of Mezzanine Financing Companies

- Mezzanine Finance in the UK

Source of the article : Wikipedia